Published: March 2026

Author: Amergin Consulting Ltd.

Target Audience: Business Owners, Small Business Seeking Financial Stability, Entrepreneurs, Start-Ups, Irish SMEs

Book a meeting: https://calendly.com/amergin-group_free/30min-finance-consultation

Major regulatory reforms rarely settle immediately after launch.

Even when legislation has been discussed for years and employers have been warned well in advance, the first few months of implementation often reveal how prepared systems actually are. Early operational realities begin to replace policy expectations.

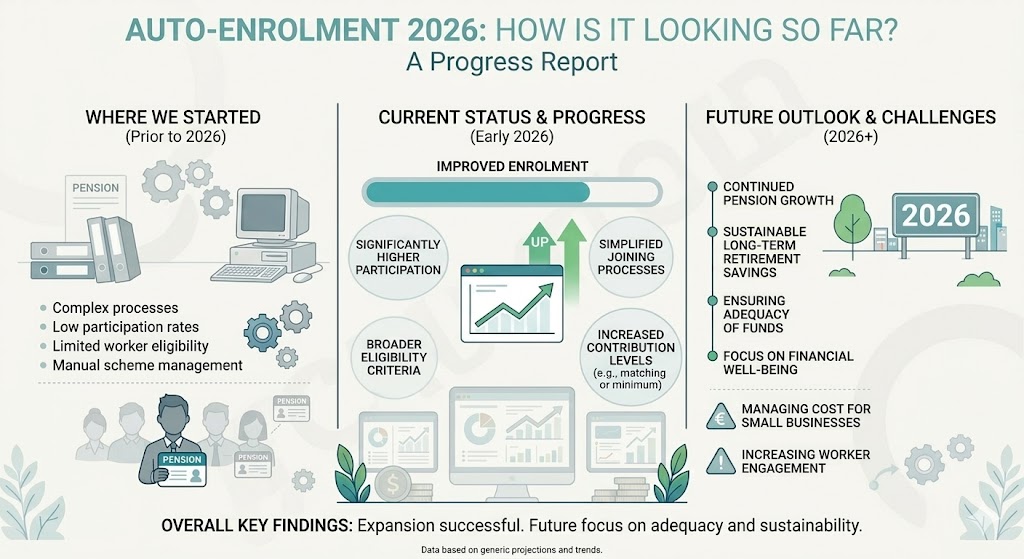

Ireland’s new Auto-Enrolment pension system, known as My Future Fund, officially launched on 1 January 2026. The scheme aims to dramatically increase pension participation by automatically enrolling workers who are not already saving for retirement through their workplace.

Three months into its introduction, the system is beginning to show how the reform is working in practice. For Irish SMEs, payroll providers, and employees, the first quarter of 2026 has offered early insights into both the opportunities and the operational challenges that come with a national pension reform.

Auto-enrolment represents one of the most significant changes to payroll and retirement savings in Ireland in decades. Understanding how the first months are unfolding can help businesses prepare for the longer-term impact.

Why Ireland Introduced Auto-Enrolment

Ireland has historically had one of the lowest private pension participation rates in the OECD.

A large proportion of workers—particularly those in the private sector—reach retirement relying almost entirely on the State Pension. Estimates suggest that hundreds of thousands of workers had no occupational pension coverage prior to the reform.

Auto-enrolment was designed to address this gap by making pension saving automatic rather than optional.

Under the new system:

- Employees who earn over €20,000 per year

- Are aged between 23 and 60

- And do not already contribute to a workplace pension

will be automatically enrolled into the national scheme.

The pension fund called My Future Fund is supported by contributions from three sources:

- the employee

- the employer

- and the State.

This shared contribution structure aims to make pension saving more accessible while distributing responsibility across workers, employers, and government.

The Contribution Model in the Early Phase

One of the most important aspects of the system is its phased contribution structure.

The scheme begins with relatively low contribution levels to ease the transition for employers and employees. In the early stage of the scheme:

- employees contribute 1.5% of their gross pay

- employers match this with 1.5%

- the government adds a smaller top-up contribution.

These contribution rates are scheduled to increase gradually over a ten-year period until the combined contribution reaches approximately 14% of salary.

This gradual scaling is intended to allow businesses especially SMEs to absorb the cost without immediate financial shock.

The Administrative Infrastructure Behind the Scheme

The scheme is administered by the National Automatic Enrolment Retirement Savings Authority (NAERSA), a new public body responsible for managing enrolment, collecting contributions, and administering pension funds.

Employers interact with the system primarily through payroll reporting. Payroll data supplied to Revenue is used to identify eligible employees and trigger enrolment notifications.

For employers, this means the operational burden of auto-enrolment sits largely within payroll processes.

Businesses that already operate structured payroll systems have generally experienced a smoother transition than those with informal processes.

What the First Three Months Have Revealed

The first quarter of implementation has highlighted several trends that are beginning to shape how the scheme will function long-term.

1. Payroll systems are the critical operational layer

The largest practical impact of auto-enrolment has been on payroll systems.

Businesses have needed to update payroll software to:

- track eligibility thresholds

- apply contribution calculations

- manage opt-out periods

- report deductions accurately

Companies that had already modernised payroll processes found these adjustments manageable. Those relying on manual payroll processes have experienced more friction.

Auto-enrolment has effectively accelerated the need for payroll system maturity.

2. Employer awareness remains uneven

Despite years of policy discussion, many organisations entered 2026 only partially prepared.

Recent surveys suggest that a large proportion of Irish organisations reported being only partly prepared for auto-enrolment prior to launch.

This has been particularly true among smaller businesses where payroll, compliance, and financial planning responsibilities are often handled by a small team.

The first months of the scheme have therefore involved a period of operational adjustment as employers adapt processes and clarify responsibilities.

3. Existing pension schemes are being reviewed

Businesses that already provide occupational pension schemes have spent the early months reviewing whether their plans qualify as an alternative to the national system.

Employers whose schemes meet certain minimum contribution thresholds can continue operating their own pension arrangements rather than enrolling employees in My Future Fund.

This has prompted many companies to revisit their pension offerings, particularly where contribution levels were previously minimal.

4. Employee understanding is still developing

Auto-enrolment has introduced pension contributions for many workers who previously had no private retirement savings.

For some employees, this has meant seeing deductions on their payslips for the first time.

While the system allows employees to opt out after six months, the early months have involved significant communication efforts from employers explaining how the scheme works and why it exists.

Clear communication has proven essential to avoid confusion.

The Financial Impact on SMEs

For most small and medium-sized businesses, the biggest concern has been cost predictability.

Employer contributions under the scheme represent an additional payroll expense. Although the starting contribution rate is modest, it will rise gradually over time.

For businesses with large workforces, the cumulative cost will become more significant as contribution rates increase.

This is why financial planning has become a key part of auto-enrolment readiness. Payroll obligations must now include pension contributions as a recurring structural cost.

Why the First Months Matter for the Long Term

The early months of any regulatory reform reveal more about its operational reality than years of policy discussion.

For auto-enrolment, the first quarter has confirmed several important truths:

Payroll systems are the backbone of the scheme.

Employer preparation levels vary significantly.

Employee education remains essential.

Financial planning must incorporate pension contributions.

The reform is unlikely to disappear or reverse. Instead, the system will mature as businesses adjust processes and employees become familiar with the structure.

Over time, auto-enrolment is expected to normalise workplace pension participation across Ireland.

What SMEs Should Focus on Now

For Irish SMEs, the early phase of auto-enrolment provides an opportunity to strengthen the systems that support compliance.

Businesses should focus on:

- reviewing payroll processes for accuracy and automation

- confirming eligibility identification systems

- ensuring pension contributions are reflected in financial forecasts

- communicating clearly with employees

- maintaining documentation of compliance procedures

Auto-enrolment is ultimately a payroll and financial discipline issue as much as a regulatory one.

Companies with strong financial systems will find the transition significantly easier.

How Amergin Supports Businesses During the Transition

Amergin works with Irish SMEs to integrate regulatory changes into structured financial systems.

Payroll processes are reviewed and strengthened. Compliance calendars ensure pension obligations are tracked alongside tax deadlines. Financial planning models incorporate employer contribution costs. Advisory support helps businesses communicate clearly with employees.

This integrated approach ensures regulatory change does not destabilise operations.

Instead, it becomes part of a disciplined financial framework.

The Bigger Picture

Auto-enrolment represents a fundamental shift in how retirement savings work in Ireland.

For decades, pension participation depended largely on individual initiative or employer generosity. The new system establishes pension saving as a default expectation for the workforce.

While the first months of implementation have required adjustment, the long-term goal is stability: a workforce that enters retirement with stronger financial security.

For businesses, the key lesson from the first three months is clear.

Compliance systems that are designed intentionally will absorb regulatory change far more easily than those built reactively.

The Takeaway

Three months into Auto-Enrolment 2026, the system is still settling into place.

The scheme has begun enrolling eligible employees, payroll systems are adapting to contribution calculations, and businesses are adjusting financial planning to incorporate new obligations.

The reform will continue evolving, but one thing is already clear.

Auto-enrolment is not just a pension policy.

It is a payroll, compliance, and financial planning change that will shape how Irish businesses operate for decades.

About Amergin Consulting Ltd.

Amergin Consulting Ltd. is a Dublin-based chartered accountancy and business advisory firm serving Ireland’s SMEs and growth companies across construction, technology, professional services, and renewable energy.

We specialise in Accounting, Payroll, Taxation, and CFO Services that help businesses build stronger foundations for profit and compliance.

Need help running a year-end tax review or planning your 2026 changes?

Amergin Consulting’s finance and tax team can help you identify deductions, forecast cash flow, and ensure full compliance before the year closes.

Book your 30-minute FREE consultation: https://calendly.com/amergin-group_free/30min-finance-consultation

Disclaimer

This article is for general informational purposes only and does not constitute financial or tax advice. While every effort has been made to ensure accuracy, legislation may change upon enactment of the Finance Act 2025.

Public should seek professional advice tailored to their specific circumstances before acting on any points discussed.

Sources and Resources

Department of Social Protection – Auto-Enrolment Retirement Savings System

https://www.gov.ie

Citizens Information – MyFutureFund Auto-Enrolment Pension Scheme

https://www.citizensinformation.ie

Revenue Commissioners – Employer Payroll and Reporting Obligations

https://www.revenue.ie

Pensions Authority Ireland – Workplace Pension Guidance

https://www.pensionsauthority.ie

KPMG – Auto-Enrolment Pension Contribution Requirements

https://www.kpmg.ie